Economic Problem of Scarcity

Scarcity is the unlimited wants and needs of consumers, combined with limited resources that producers have. People have unlimted wants and needs, so everyone can't be satisfied without an unlimted amount of resources. Unfortunatley, there is a limited amount of resources, so tradeoffs must be made. This is one of the biggest problems in society. Just because someone wants something, that doesn't mean that person will get it because of scarcity.

Concept of Supply and Demand

Supply is the amount of goods and services that producers will provide at various prices. Profit is neccessary because otherwise producers lose money. Demand is the amount or quantity of goods and services that consumers are willing to buy at various prices. Higher prices result in less buying by the consumer while lower prices result in more buying by the consumer. Price is involved with the concept of supply and demand because when the quanitity of a product demanded is the same as the quantity supplied that point is the equilibrium price or market price.

Types of Economic Competition

-Pure competition is where many suppliers offer very similar products (Example: Agricultural products such as corn or wheat is easy to find at a grocery store, and price is a big factor). The graph is a horizontal line.

-Monopoly is a typle of market in which one supplier offers a unique product (Example: Monopolies aren't common in the United States because of government control. Without government restictions, gas could be a monopoly). The graph is a vertical line.

-Oligopy is where a few businesses offer very similar products or services (Example: The airline industry is an oligopy because there are a limited amount of airlines companies). The graph has a slightly negative-looking slope.

-Monopolistic competition is where there are many firms competing with products that are somewhat different (Example: Athletics clothes would be involved in monopolistic competition because there are many types of styles. Differences would be comfort, apperance, physical shape, etc). The graph has a slightly negative-looking slope for products with few differences, and increases with greater product differences.

-Monopoly is a typle of market in which one supplier offers a unique product (Example: Monopolies aren't common in the United States because of government control. Without government restictions, gas could be a monopoly). The graph is a vertical line.

-Oligopy is where a few businesses offer very similar products or services (Example: The airline industry is an oligopy because there are a limited amount of airlines companies). The graph has a slightly negative-looking slope.

-Monopolistic competition is where there are many firms competing with products that are somewhat different (Example: Athletics clothes would be involved in monopolistic competition because there are many types of styles. Differences would be comfort, apperance, physical shape, etc). The graph has a slightly negative-looking slope for products with few differences, and increases with greater product differences.

Types of Economic Utility

-Form results from changes in the tangible parts of a product or service (Example: A shoe could get more support and a new style).

-Time results from making the product or service available when the customer wants it (Example: A store could be open twenty-four hours per day).

-Place is making products or services available where the consumer wants it (Example: There could be faster shipping to home).

-Possesion results from the affordablility of the product of service (Example: The product could be purchased with a credit card).

-Time results from making the product or service available when the customer wants it (Example: A store could be open twenty-four hours per day).

-Place is making products or services available where the consumer wants it (Example: There could be faster shipping to home).

-Possesion results from the affordablility of the product of service (Example: The product could be purchased with a credit card).

How Marketers Use Utility to Increase Customer Satisfaction

Economic utility is the amount of satisfaction a customer receives from the consumption of a particular product or service. Marketers use utility as a marketing tool because it supports the marketing concept. It is effective when a business uses utility to develop a marketing mix to focus on unique needs of each target market. When economic utility is improved, customer satisfaction is as well.

Business / Economic Cycle

The business cycle starts with expansion, goes into recession and trough, and ends with recovery.

-Expansion is where unemployment is low, consumer confidence and spending are high, and businesses invest in product development and research and development. The government increases taxes.

-Recession is when expansion peaks, and the economy slows. Businesses lay off workers and consumer spending is low resulting in less money to invest. The government lowers interest rates.

-Trough is the low point of the business cycle. The economy stops slowing, and there are signs of a recovery. The government reduces interest rates, cuts taxes, and institutes federally funded programs.

-Recovery is where the economy begins to grow. Jobs are created and it is similar to the expansion. This period can last a long time. The government increases taxes.

-Expansion is where unemployment is low, consumer confidence and spending are high, and businesses invest in product development and research and development. The government increases taxes.

-Recession is when expansion peaks, and the economy slows. Businesses lay off workers and consumer spending is low resulting in less money to invest. The government lowers interest rates.

-Trough is the low point of the business cycle. The economy stops slowing, and there are signs of a recovery. The government reduces interest rates, cuts taxes, and institutes federally funded programs.

-Recovery is where the economy begins to grow. Jobs are created and it is similar to the expansion. This period can last a long time. The government increases taxes.

Resources & Goods / Services

-Natural- Land includes everything contained in the earth or found in the seas. Land is a natural resource.

-Labor- Labor refers to all people who work. They are paid to make the goods and services.

-Capital- Capital includes money to start and operate a business. It includes things used to produce goods and services.

-Entrepreneurial- Entrepreneurship refers to the skills of people who are willing to invest their time and money to run a business. They are people who recognize opportunities and start businesses.

-Labor- Labor refers to all people who work. They are paid to make the goods and services.

-Capital- Capital includes money to start and operate a business. It includes things used to produce goods and services.

-Entrepreneurial- Entrepreneurship refers to the skills of people who are willing to invest their time and money to run a business. They are people who recognize opportunities and start businesses.

How Economies Are Measured

-Productivity is output per worker over a defined period of time, such as a week, month, or year.

-Gross Domestic Product (GDP) is the output of goods and services produced by labor and property located within a country.

-Gross National Product (GNP) is the total dollar value of goods and services produced by a nation, including goods and services produced abroad by U.S. citizens and companies.

-Standard of living is a measurement based on many factors inlcuding education and health care.

-Inflation rate refers to rising prices.

-Consumer price index (CPI) measures change in price over a period of time of some 400 specific retail goods and services used by the average household.

-Producer price index measures wholesale price levels in the economy.

-Gross Domestic Product (GDP) is the output of goods and services produced by labor and property located within a country.

-Gross National Product (GNP) is the total dollar value of goods and services produced by a nation, including goods and services produced abroad by U.S. citizens and companies.

-Standard of living is a measurement based on many factors inlcuding education and health care.

-Inflation rate refers to rising prices.

-Consumer price index (CPI) measures change in price over a period of time of some 400 specific retail goods and services used by the average household.

-Producer price index measures wholesale price levels in the economy.

What is the Difference Between Macro- & Microeconomics?

Macroeconomics is the study of the economic behavior and relationships of an entire society while microeconomics examines relationships between individual consumers and producers. Microeconomics is similar to the market for a product.

Questions All Economies Have to Answer

1. What goods and services will be produced?

2. How will they be produced?

3. For whom will they be produced?

2. How will they be produced?

3. For whom will they be produced?

Types of Economic Systems

-Market economies are where decisions are made in the marketplace.

-Command economies are where a central authority makes the key economic decisions.

-Mixed economies contain both private and public enterprises.

-Command economies are where a central authority makes the key economic decisions.

-Mixed economies contain both private and public enterprises.

Characteristics of Private Enterprise

-Private enterprise is based on independent decisions by businesses and consumers with only a limited government role regulating those relationships.

Characteristics would include resouces owned by the producers, producers incorporating the profit motive, consumers consuming based on value, and the government staying out of the way of the business.

Characteristics would include resouces owned by the producers, producers incorporating the profit motive, consumers consuming based on value, and the government staying out of the way of the business.

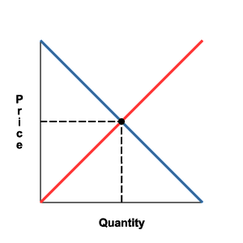

Law of Demand/Supply & Demand/Supply Curve

-Law of demand is when the price of a product is increased, less will be demanded.

-Law of supply is when the price of a product is increased, more will be produced.

*Graph key

Demand curve = blue line

Supply curve = red line

-Law of supply is when the price of a product is increased, more will be produced.

*Graph key

Demand curve = blue line

Supply curve = red line